When getting a mortgage we often wonder how do we get started on this process? Seems like it can be a confusing process when it’s your first time every buying a home..

First Step To Getting Start With Getting a Mortgage Loan.

We are going to discuss in details the process you need to take to successful get your home loan approved. One of the most important steps when your trying to get your loan approve is you have to make sure you check your credit report.

Sense This can easily be done these days on your mobile phone. You can check your credit using Creditkarma.com,

Another good resource to check your credit would be experian.com

You can also check out your other credit report on https://www.transunion.com/

If you are on a tight budget and you want a free copy of your credit report you can go to Annualcreditreport.com and get a free copy of your credit report too.

Once this is done you can go thru the report and see what things you need to have removed from your credit report. A lot of time you can call up the creditors and debt settle with them. You can either do that or send out verification letters getting them to verify the debt and if for some reason they can’t verify the debt they will have to remove the information from you credit report. We will have more on this in a different article.

Looking Around For The Right Mortgage Company

Once you know what your credit score is then its time to look around for the right mortgage company. The main thing you want to pay close attention to is how many points are being charged and what are the closing cost. Most of the time these points fall around 1 or 1 1/2 points or even 2 points depends upon the market rate and it also depends upon the lender you choose. A few years ago there were ways that you could buy down your points to lower your interest rate.

The only thing is that sometimes you would need to weigh out does buying down your points actually save you money in reference to the interest rate… Typically when you look at the interest rate if you have a interest rate of 3.5% vs 3% you would normal see like a $20 or $30 difference in monthly payment. Now if you look at the amortization over the course of the years this might show you were the saving is over the course of a 30 year loan or 20 year loan. But you would have to weigh this out and see what you want to do.

https://bettermoneyhabits.bankofamerica.com/en/home-ownership/buying-mortgage-points-lower-rate

You might be better off taking the same money and putting it in something else and having it yield you a better return. Be sure to consult with your Lender and Professional adviser in reference to this part.

The average closing cost is around 3 percent to 6 percent of whatever the loan amount is. If you look hard enough you can even find someone who has very low closing cost which will save you money when it time to purchase the home you qualify for…

Hunting For The Right Lender

When you are hunting for the right loan its time to make sure you are working with a good lender… You want to make sure that this lender will be able to close your file in a timely manner. You will be surprised at how many home sales fall thru because the Buyer’s lender failed to get something upfront, or they failed to inform you on missing paperwork or they failed to tell you how to insure that your debt to income ratios stay the way that they are until you close your file. Remember, if you are getting a loan you want to make sure that you do not increase your debit to income ratio.

Here is a question you want to ask your potential lender “If I was to go with your company how soon will you be able to get my loan closed?” This is the first question you want to ask the lender. Your goal is to make sure you have a lender that can close your file in a timely manner.

You also want to ask the lender what types of programs do they have for first time home buyers. Remember if you are having issues not having enough down payment there are programs like TSAHC and Seth that are available to help you with closing cost.

You can also ask them if they participate in any bond programs. Another thing if you are buying a house in rural areas you can see if the area qualifies for USDA Loan Program.

One other program to ask them is if they do 203k FHA loans.. These 203k FHA loans are loans used to help you get in a home that needs work. Some lenders are in this program and others are not. This is why you want to ask when you are interviewing for your lender do they know about these programs.

The Application Process

Once you’ve identified with the lender you want to use, then its time to fill out an application. This is normally handle with a online form or a over the phone application and from there the lender will give you what we call a pre-approval letter. (note: the best thing to get is an actual full approval this is when you get all paperwork into the lender. The paperwork normally will consent of your w-2 or tax returns, retirement accounts and if you are receiving a gift from your mom or dad, etc you will need to show exactly were the gift funds come from. If you are self-employed it would normally be 12 months bank statements possibly required to show were your income comes from etc.

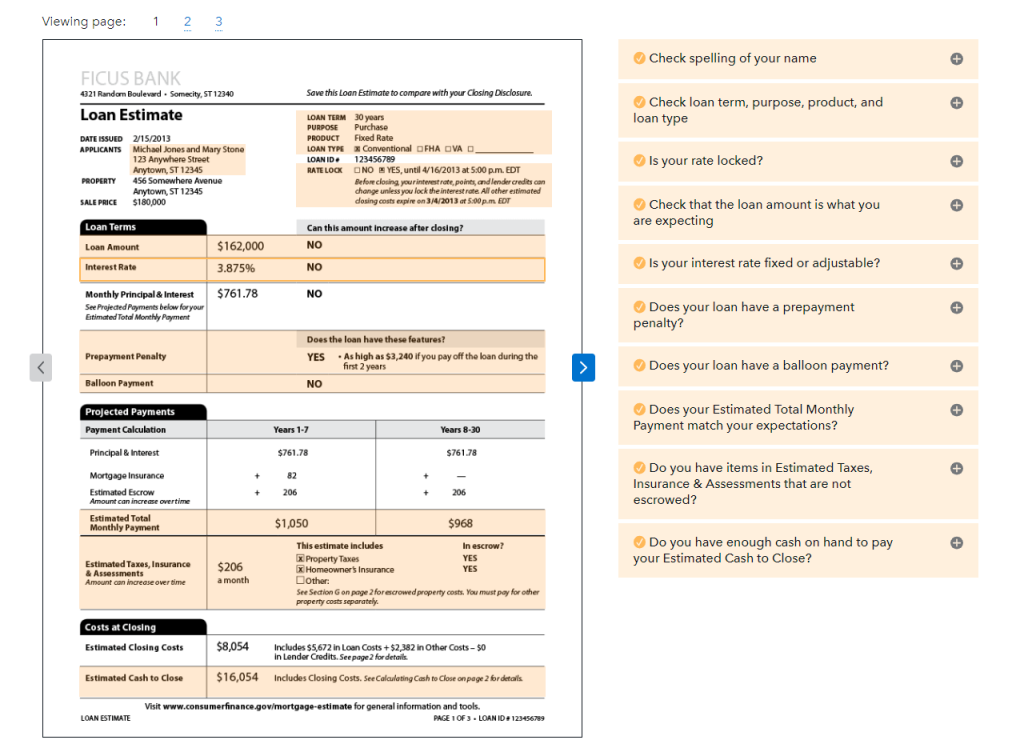

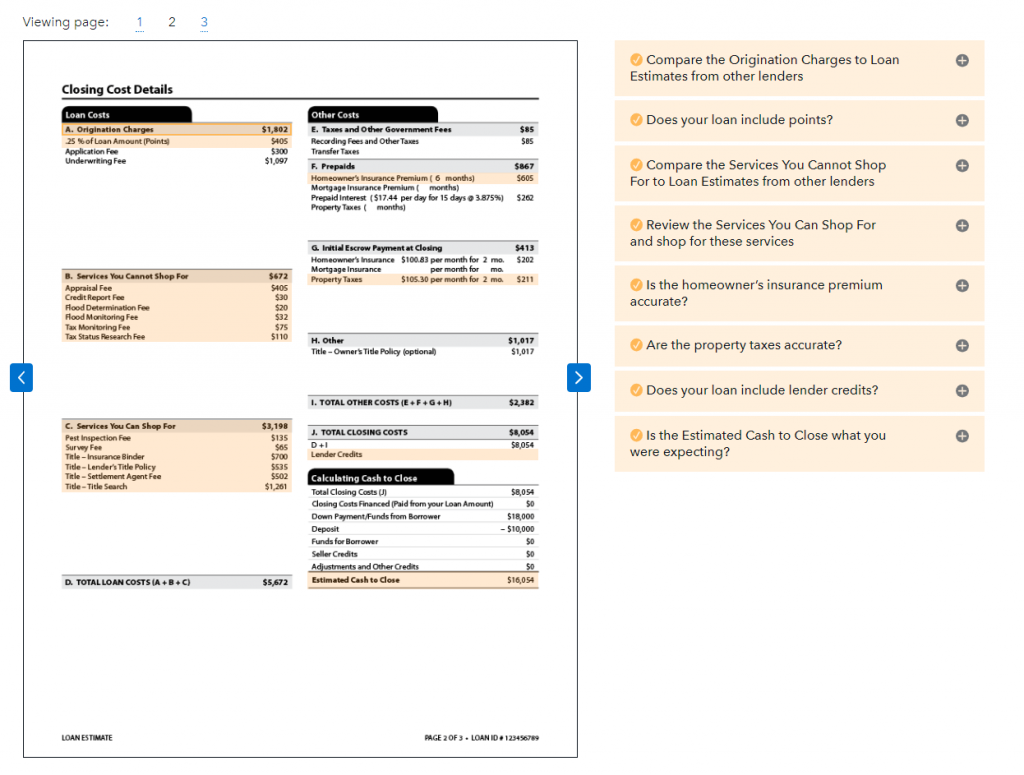

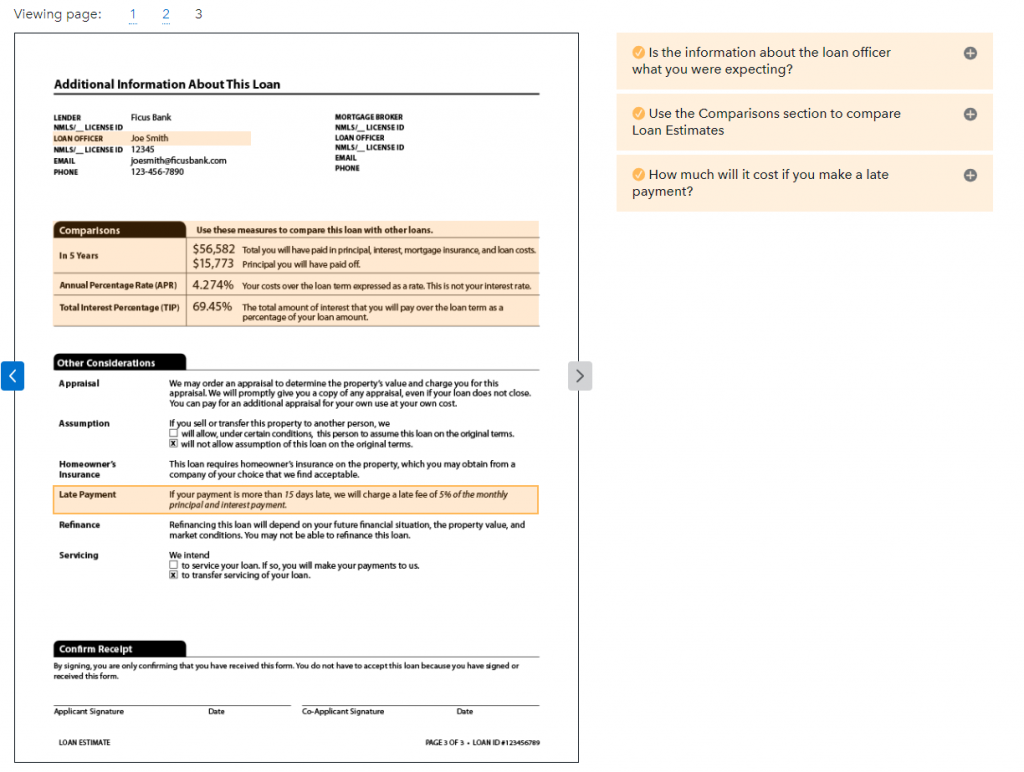

Another important form to pay close attention to is the good faith estimate referred to now as the Loan Estimate. The Loan Estimate is the form that you will receive that will break down your cost of the loan.

This form is suppose to be given to you in a timely manner, normally within 3 days.. This form has the lenders breakdown of all lender fees, etc..

https://www.consumerfinance.gov/owning-a-home/loan-estimate/

https://www.consumerfinance.gov/owning-a-home/loan-estimate/

https://www.consumerfinance.gov/owning-a-home/loan-estimate/

Time To Work With A Realtor

At this point, it’s time to work with A Realtor. You want to make sure that you go through getting your loan first before working with a Realtor. Once you are ready. The Realtor will be able to show you properties. You will show the Realtor your approval letter upfront. This lets the Realtor know that you are serious about buying a home

Please keep in mind, the Realtor is a professional. You have to respect their time as well. When you are approved first, this ensures that time will not be wasted. So many people do the process of looking for the house first without getting approved or without having a letter.

When you do the process this way. You are also saving yourself time because you know exactly how much you able to purchase. Also, you might not want to buy a house for the full loan amount. You might want to buy a home for a lower loan amount which will also save you money in monthly payments as well.