So you need to do a forbearance plan and you have no idea where to start. Then this is going to be a must-read article for you.

The thing about the forebearance plan is that it is an idea for someone who has just lost their job or lost their income and has no way of paying their mortgage.

When dealing with a crisis as Covid-19 no one saw this type of crisis coming. And due to this crisis, it causes a repeal effect to happen.

One minute we find that we were doing just fine and living our lives and enjoying the fruits of our labor.

And the next minute we now find ourselves dealing with how we are going to pay the bills. As we listen to the news media we often wonder where do we go from here.

If you found yourself getting behind on your mortgage payments and you have no idea what you need to do next then you need to keep reading this article.

We are going to be talking about what you need to do if you find yourself falling behind on the mortgage payments.

We are going to also talk about what some of the forbearance agreements look like from bank to bank. So we are going to look at a few different banks and get a better understanding of what the banks are looking for you to do a forbearance agreement.

We will also look at what happens after the next few months and what you need to understand about how this forbearance plan is going to work.

Once you get a better understanding we are going to then go into a few details of what you will need to do next once you are done with the forbearance period.

Understand what is a forbearance

Before we get started we need to get a better understanding of what is forbearance. Many people get forbearance agreements and loan modifications mixed up. Let’s take a look at the definition of a forbearance agreement.

Understand that a forbearance agreement is when a lender allows a homeowner to skip monthly mortgage payments or pay an adjusted amount for a short period.

Any unpaid interest or late penalties are normally added to the principal of the loan. The lender agrees with the borrower to stop all foreclosure activities during this period.

So the lender will allow you to pause your payments for a limited period of time. What this does is it allows the homeowner an opportunity to recover from a temporary setback while being able to stay in their home and keep there home.

Most mortgage lenders will require homeowners to complete a form. But remember every lender is going to be different on how they are doing their forbearance process.

There are two types of forbearance plans. You have one for a temporary hardship and then you have one for a permanent or long-term hardship.

A temporary forbearance helps gives the homeowner a temporary reduction on payments or it helps suspense the monthly payments for your home loan for a while. This allows you a chance to cure any delinquent payments.

What this means is you will be asked to make a significantly reduced payment for a while or in some cases you might make no payments at all.

The idea behind this is it allows you an opportunity to get past a temporary hardship. It also allows you a chance to get back on your feet and resume making your normal payments.

The length of time that your payments will be reduced or waived can be from 3 months or more. Depending on what your lender has set up.

Fоr example: If your mortgage payment is $2500 a month and you missed three months’ payments, the lender may require you to begin making additional amounts along with your monthly payment. The additional amount is then applied towards the missing payments until the missing payments are cleared up which brings the mortgage loan back current.

Other forbearance agreements allow the borrower to stop making monthly payments altogether for a fixed period.

What this does is allow the borrower time to get back on his or her feet. Any missed mortgage payments and interest are added to the loan principal balance.

The normal terms of the mortgage then go back into effect once the monthly mortgage payments begin again.

What are some of the advantages and disadvantages

So what would be the advantages and disadvantages of doing a forbearance? One of the best advantages of doing forbearance agreements is it helps you to avoid foreclosure and it allows you an opportunity to remain in the property.

The second advantage of doing a forbearance is it gives you more time need to come up with the missing payment amounts.

If you have no job right now then your not bring in any income. And when you do the forbearance it gives you some time to get caught up. And right now a lot of people need time. They need a chance to get back on their feet.

Another advantage of doing a forbearance is being able to avoid a foreclosure. When you do a forbearance agreement it helps you to avoid being in foreclosure.

Also if for some reason if you don’t have your job yet or your out of work you can see if your mortgage company is offering an extension on the forbearance agreement.

The disadvantage of the forbearance agreement would be having to catch up on the amount at a later time.

So at some point, the amount will be due and payable. Forbearance does not erase what you owe. You’ll have to repay any missed or reduced payments in the future.

If you are able to keep up with your payments then you shouldn’t be doing a forbearance agreement. But this all depends on the mortgage lender and the different programs that are set aside for Covid-19.

Right now if you have no income coming and you know you’re not going to have any income coming in within the next 2 to 3 months then doing the forbearance agreement will help your situation.

Because it allows you a chance to stay in your property while you’re looking for some way to subsidence your income to begin making payments again.

What provision is provided for FHA, VA, USDA, Fannie Mae, and Freddie Mac loans

You should now have a better understanding of what is a forbearance agreement. You do know that doing a forbearance does not erase what you owe. You’ll have to repay any missed or reduced payments sometime in the future.

If your mortgage is backed by the federal government this includes FHA, VA, USDA, Fannie Mae or Freddie Mac loan provisions of the recently enacted Cares Act allow you to temporarily suspend payments if you are experiencing financial difficulty due to the impact of the coronavirus on your finances.

Your mortgage company may also have forbearance or deferment options for non-government backed or privately held loans, but the extra options available to you may be different. So you will need to contact your lender to find out what these options are.

Under the Cares Act which is federally backed mortgage loans if you are experiencing financial hardship due to the coronavirus pandemic, you have a right to request forbearance up to one hundred eighty days. You also have a right to request an extension for up to an additional one hundred eighty days.

In order to get this done, you must contact your loan servicer to request this forbearance. There won’t be any additional fees, penalties, or interest added to your account to do this. But the regular mortgage interest will still be charged.

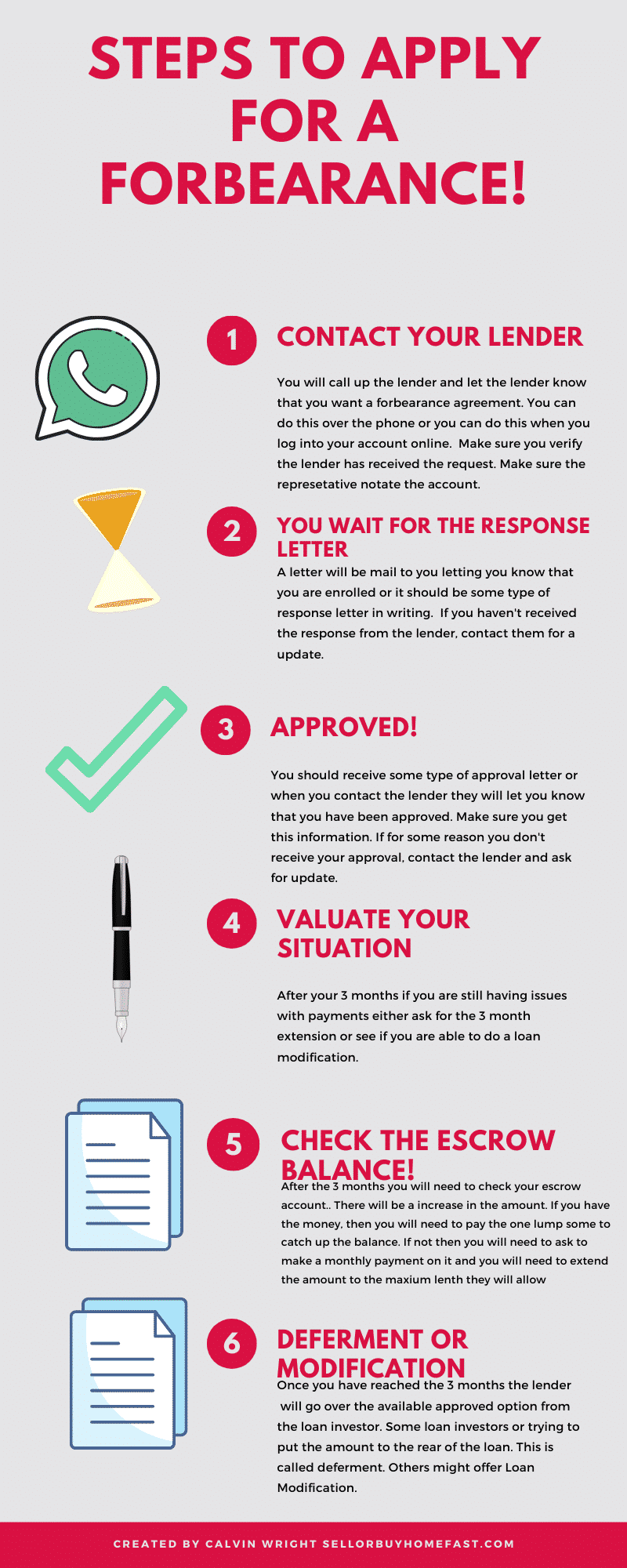

How to apply for the forbearance

To apply for the forbearance agreement most mortgage companies have made this process a very easy process. Unlike having a lot of paperwork in the past.

All you mostly need to do is pick up the phone and give them a call, or apply online or they might have an automated phone system that helps you apply for the forbearance.

You won’t need to submit any additional documents, You want have to come up with paystubs or other paperwork or any additional documentation to qualify.

All you need to do call them and say your having issues making payments due to the pandemic and you want to do the forbearance plan or, you want to ask them what relief they have available.

Wells Fargo Bank Forbearance Plan

We are going to take a look at Wells Fargo’s phone:800-219-9739 and go over what they are offering. Wells Fargo Forbearance Plan is going to work as follows:

- 3 Months with no recourse

- no late fees

- Payment is suspended for 3 months

Note: You will receive a mortgage letter in the mail once you have finished applying.

There will be no negative reported to the Credit Report for those 3 months. The missed payment will be set based on the guideline of the bottom line loan investor.

One thing to keep in mind that the actual payment missed will be in principal and interest. The escrow will not be accounted for.

So what this means is they are going to suspend the principal and interest the taxes and insurance will still be added up each month and this will result in the shortage of escrow.

So at the end of the 3 months, you will need to contact the escrow department and find out from the escrow department how much escrow is owed.

From there you will then either pay the escrow amount or the escrow amount will be spread-ed out… You want this amount spread-ed out for the maximum amount allowed. If they will do it for 2 years then extend that amount for the 2 years.

For example: If for some reason you are short $2,000 in your escrow account but the bank will give you up to 2 years to repay the amount back then this would be 83.33 extra added to your monthly mortgage note.

You would extend out the payment for the longest amount of time allowed then within the 2 year period when you have enough money available you would go back to your mortgage lender and pay off the owed amount.

After that, you would contact the escrow department and have them run a re-analysis of your escrow account. This will then take off the additional monthly payment amount.

If you intend to refinance you must make sure that your forbearance amount is caught up before you do a refinance down the road. So that means you must resolve the forbearance amount before you can refinance.

If you need additional time beyond the 3 months Wells Fargo has additional options available which will include continuing of a payment suspension.

Moving the missed payment to the end of the loan or doing a loan modification. For more information on options after the 3 months contact Phone 877.613.6079.

Chase Forbearance Plan

We are going to take a look at Chase Forbearance Plan phone is: 1.800.848.9380 and go over what they are offering. Chase Forbearance Plan is going to work as follows:

- 90 days protection or forbearance with no recourse

- no late fees

- Payment is suspended for 90 days

Note: You will receive a mortgage letter in the mail once you have finished applying.

There will be no negative reported to the Credit Report for those 90 days. The missed payment will be set based on the guideline of the bottom line loan investor.

There will be a shortage in the escrow account. So once the 90-day suspension is over you will need to contact Chase escrow department and ask them about the shortage amount that due.

You can then make arrangements to pay the shortage amount in one lump sum or spread out payments for a period of time. Make sure you get this for the maximum amount of time allowed.

Once the 90 days have ended there is some discussion about deferring the 90-day amount to the end of the loan. If you have an FHA or Fannie Mae or Freddie Mac then their guidelines will apply to what will happen after the 90 day period.

You can also get an additional extension if for some reason you need additional time. Also, Loan Modification is also an option after the 90 days period has ended and if you reached the 90 days and need help with the loan modification then contact me. I will be able to assist you in getting the loan modification done.

Bank of America Forbearance Plan

We are going to take a look at Bank of America Forbearance Plan phone is:800.669.6650 and go over what they are offering. Bank of America Forbearance Plan is going to work as follows:

If you are only one payment behind then they are going to put you in a plan called The Bank of America Payment Deferral Program. This program works like a forbearance plan but it is only when you are one month behind.

The Bank of America Payment Deferral Program is as follows:

- defer 3 months payments – This means they will put the payment to the end of your note ( This would allow you a chance to just make normal payments without being behind)

- no late fees

- If for some reason you not able to make a payment after the 3 months they will extend it out another term

- Payment is suspended for 90 days

- This offer will depend on the investor of the loan

- The bank will continue to pay taxes and insurance but note that it could cause a possible shortage in the account.

- If you are awarded this plan its possible that the taxes and insurance deferment will be included in the deferral and will be placed at the end of the loan. You will need to talk to a representative at the bank in reference to this.

The Bank of America Payment Forbearance Program is as follows:

- This program is will be used when if for some reason the investor of the loan doesn’t approve you for the deferral program

- They will do a forbearance period for 90 days

- No late fees

- No Negative markets on credit for 90 days

- They will continue to pay the escrow of your taxes and insurance but you will possibly have a shortage in the account at the end of the 90 days and will need to contact the bank to find out your option on a repayment plan or try to pay the shortage in 90 days.

Note: You will receive a mortgage letter in the mail once you have finished applying.

If you have a Fannie Mae, Freddie Mac, FHA they are going to go off what Fannie Mae and Freddie Mac say. More than likely they will give you the 90-day suspension and then they are going to either defer the payments to the end of the loan or they will offer you a loan modification. If you need help after the 90 days with the loan modification then contact me.

Mr. Cooper Home Loan Forbearance Plan

Mr. Cooper Home Loan Forbearance Plan Phone is:888-480-2432 is as following:

- Forbearance Agreement Plan

- Payment suspension for 90 days

- No Late Fees

- No negative marks on the credit report for the 90 days

The escrow will continue to get paid on the taxes and insurance but at the end of the forbearance, you will need to contact them to see where you are in reference to the amount that is owed.

At the end of the 90 days you will need to contact them and speak to them about prepayment options.

More than like you can do a lump sum payment amount. You can also be able to spread out the mess payments for the maximum amount provided by Mr. Cooper. When you do it like this you can then ask can you pay back the amount early.

The other option that they are offering is Loan Modification. If you need any assistant when this time comes to put together your loan modification contact me.

When you do the Loan Modification you are modifying the loan so this should allow you a chance to catch up completely and you will just make payments like you normally would to your loan company.

ShellPoint Mortgage Forbearance Plan

ShellPoint Mortgage Forbearance phone is: 800.365.7107 is as following:

- The forbearance plan period is averaging between 2 months to 3 months. If you need longer time you can contact them and let them know

- no late charges

- no negative credit reports during the duration of the agreement and possible longer

Once you are done with the 2 to 3 month period if your needing additional time you may be able to ask for an extension. If you don’t need any more time and you are back on your feet then the amount that is owed will go as follows:

- Deferment of the amount owed. That means the amount will be put to the end of your loan.

- Repayment plan option. If you end up with this option the repayment amount can average around 16 months to 24 months. For example, if for some reason you owe $8,000.00 at the end of the forbearance and you not able to get a deferment option the amount owed will be $500.00 additional on top of the normal mortgage amount. If you get the 24-month option to repay the amount owed then the amount will be 330.00 additional add to your monthly payment.

- Restatement would be to just pay off the amount that is owed on the forbearance.

The escrow account will be paid but there will be a possible shortage in the escrow account. The option of paying the shortage amount will be as following:

- You can ask to just pay interest on the amount

- You can pay interest and escrow amount

- You can pay nothing and have this amount split into payments which can be spread for the maximum amount the bank allows or you might get the deferment and this amount will be put to the end of the loan.

Shellpoint Mortgage will send you approval information through the mail.

Conclusion:

Hopefully, you have a better understanding of what the forbearance plan offers. You want to make sure that you have a full understanding of what the forbearance plan is.

Also, you want to be careful listening to Youtubers or people who tell you not to take this plan. This plan is designed to help you stay out of foreclosure and it is also designed to help you catch up if for some reason you are behind on your mortgage payment.

The banks are willing to offer you assistance in your time of need and these plans will eventually help you to stay out of foreclosure and allow you a chance to get things back to normal.

If you need any future assistant I’m one call away or contact your mortgage company and they will be happy to assist you.