Have you always wonder how to use the popular platform hudhomestore.com? Let face it, sometimes buying HUD properties can be a confusing process.

It takes a good understanding on what you need to know in order to successfully buy a HUD property.

We will be discussing briefly a few tips to help you when you are trying to buy a HUD property.

Search For HUD Properties

Go to the home page for HUD homes.

This would be HUDhomestore.com. Make sure you type that in correctly if you want to look at HUD homes.

If you misspell it a little bit, you might go to a different website which pretends to be HUD but is not, and might try and give you a nasty virus or something on your computer.

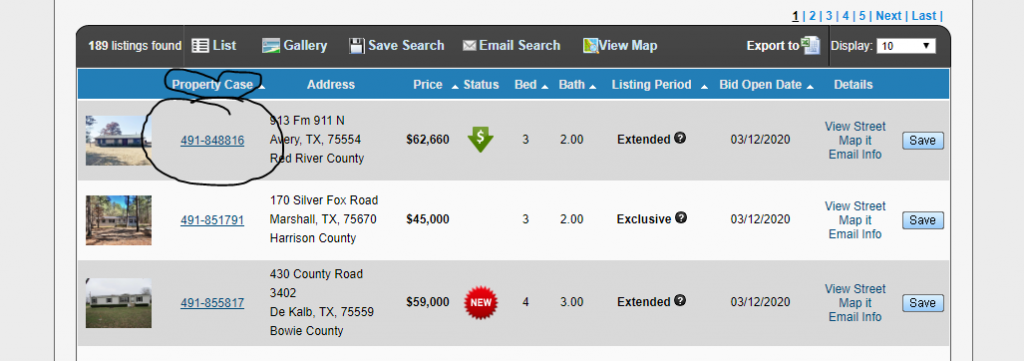

When you are there on the site there are a few ways to search for HUD homes.

You can click on the state, and see any HUD home for sale in your particular state note quite a few will pop up.

Or, you can search properties. That’s the only field that you have to enter, is the state.

And then you can enter any one of these fields to narrow down your search a little bit.

Click search, and you will see the results.

Whatever the results are in your area is what is in the HUD inventory. So what that means is they are on the market, and your able to place a bid.

They do not have a contract on them. As soon as HUD receives an acceptable bid, they will take the property off the market, or do a price change, or for some other reason, they might pull it off HUD home store.

To learn more information on the property click case number

So if you want more information on this particular property, click on the case number and it will pull up this page, which will show you more information on the property.

Break down of the bidding periods

A few things to know about HUD: they have different bidding periods for different buyers. So if you are an investor, you cannot bid on HUD homes right away.

There’s a few differences on the bidding periods. First bidding period is the FHA-insured bid period. If you look closely you will see “insured with escrow.”

That means it is FHA insured. There is a 10 day initial bid period where HUD collects all the bids and they will accept one at the end of those 10 days if it meets their guidelines.

And there’s a 15-day owner-occupant only bid period.

So for the first 15 days, only owner-occupants can bid, unless you’re a nonprofit or a government agency.

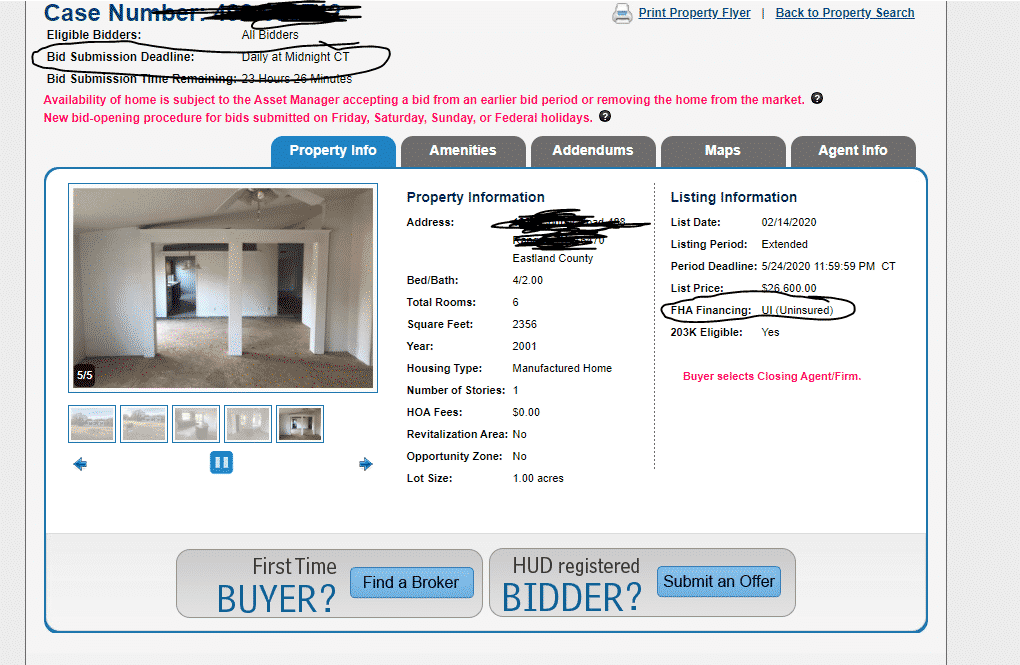

You can see in the example who is eligible to place a bid. Now you want to know when the bid submission deadline is.

This would be for the initial 10 day bid period on this property—it’ll tell you date and the time and the time remaining to submit your bid.

Once the time run out the bid submission deadline is over. So HUD takes all the bids they get, and review them all at once during this time period.

Then on the next business day they will accept one of the bids if it meets their guidelines. So they have certain guidelines, certain dollar amounts those bid have to meet.

And HUD only cares about the net price to them.

They don’t care if it’s cash, if it’s financed—it could be a 203K full-blown rehab loan versus a cash deal, and or of the 203K loan is one dollar more net to HUD than the cash deal, they will take that 203K loan.

So there’s no advantage to doing cash or a loan with HUD.

If this is FHA-uninsurable, the bidding period would be different.

There would be a five-day initial bid period for owner-occupants. And a five-day sealed bid period when they collect bids.

So HUD would take all the bids they get in those five days, look at them on the next business day, and accept one at that time if it met their requirements.

On the sixth day, investors could submit bids with an FHA non-insurable. It’ll say under the listing information if it is insured or not.

On the houses that are insured, it’s the sixteenth day after it has been actively for sale that investors can bid.

Now again, I said actively because if this home goes under contract, say on the eleventh day, as soon as it goes under contract the active days on market stops according to HUD.

For example, if it goes under contract on the eleventh day,and the buyers cancel their contract two weeks later because they found something wrong with the home, it would come back on the market as if was only for sale for 11 days.

And investors still could not bid because it has to be on the market 15 days actively until they can.

For investors to know when they can bid, you want to look at the period deadline. This is the last day owner-occupants can bid till the next day.

Now if you try to bid on it before then, the HUD system will not let you do it. Let’s talk a little bit about bidding.

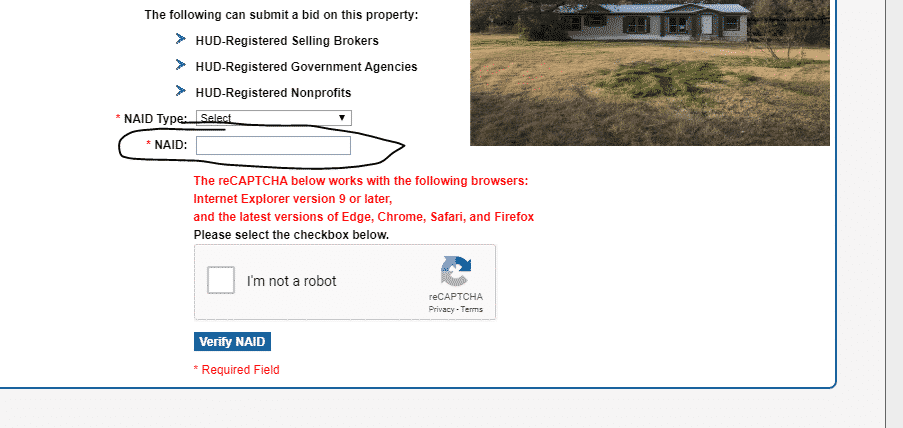

If you want to bid on a HUD home, you have to have a real estate agent submit a bid for you. Buyers cannot submit them directly.

That real estate agent has to be registered with HUD.

Your Broker or Agent has to be registered.

They have to have what is called a NAID number, or their office does, and then individual agent has to register on the HUD website, which they can do right up here very easily, takes about five minutes.

And they can register on the site. If their office does not have a NAID number, it can take four to six weeks to get it from HUD.

Right up here, it says NAID application. So if you’re a real estate agent and your office does not have one of these, you need to get one right away.

It’s free, it doesn’t cost anything, but you have to apply with them. And it will take some time to get it.

And until you have that, real estate agents cannot bid on HUD homes.

There’s no way around that. If you are agent and you have a buyer who wants to buy a HUD home and you don’t have this, you will have to refer them out to another agent, somehow get another agent to help you out who is registered with HUD.

Once you have your agent who can bid on a HUD home for you, all bids are submitted online. Technically, you don’t have to sign any contracts, provide a pre-qual letter, or earnest money to bid on a HUD home.

However, it is highly suggested that you have your earnest money and your pre-qual letter ready to go, because if your bid is accepted, you’ll have 48 hours to get it to HUD.

And that’s a real copy, not emailed, but physically delivered to HUD.

In some cases, you may have to overnight it to a different state because the HUD asset manager may be located in Texas, and you could be in California.

So if you don’t have your pre-qual letter, or your proof of funds letter, ready to go, you could have your bid cancelled if you don’t get the package in on time to HUD.

Again, your real estate agent can help you submit that package to HUD, they will assist with that process, but you need to have your pre-qual letter, your proof of funds, ready to go.

And then you’ve got to have certified funds for the earnest money. That means you can’t write a personal check.

You’ve got to have a certified check, a money order—something that proves you’ve got the money.

And that also has to be sent either to HUD or the listing agent’s office, depending on the asset manager who’s listing the house.

Again, your real estate agent can help with that once your bid’s accepted.

You need to make sure you have certified funds available, and the pre-qual letter, or proof of funds letter.

Now, how much will HUD accept?

Well, that depends on the market you’re in. It’s possible that HUD will take about 10 or 11 percent less than the list price net to them, remember every property is different.

How much will HUD possibly accept?

The word net is very important because that doesn’t mean if you offer them $135,000 they will automatically accept it, because it’s within, 10 percent, because you have to factor in the real estate agent commission, and any closing costs you want HUD to pay.

The listing agent commission is automatically 3 percent on HUD homes.

So if you’re offering, below list price, once you take out that 3 percent, HUD will accept about 7 or 8 percent less than the list price.

The buyer’s agent can make up to 3 percent on HUD homes as well. They don’t have to take that much, but they can.

So if they take 3 percent, that means you’re paying 6 percent total commission.

HUD will now take 4 to 5 percent less than the list price after you factor in commissions.

And, if you ask HUD to pay 3 percent of your closing costs, then that also is deducted. So now you’re down to 9 percent total cost HUD is paying.

You’re going to get, you know, 1, 2 percent maybe less than list price net that HUD will accept. It is also important to know HUD does not pay all the customary costs that many other sellers pay.

They do not pay title insurance for the buyer, they do not pay half the closing fee for the buyer, they do not pay to have utilities turned on for your inspections—those are all costs that the buyer incurs.

What are some of the expenses that buyer’s might have to by when bidding on a HUD property?

The buyer will have to get utilities on in their name to do an inspection.

They will have to pay any deposits, they’ll have to pay any costs or fees while those utilities are on.

It is the buyer’s responsibility to get the home de-winterized if it’s in the cold months and the home has been winterized.

And they may have to pay HUD 150 dollars to have the home re-winterized as well, after their inspection. So that 150 dollars, it’s paid before the inspection.

After your inspection is done, HUD’s company comes back in, re-winterizes the home, blows the pipes out, puts antifreeze in the toilets and P traps, makes sure the home won’t freeze again.

So there are many costs with HUD that are not there on a typical purchase. Let me go back real quick again to what HUD accepts.

We said that they possibly might accept 11 percent or something around in those lines. In some areas where there’s less competition, more REOs, they might take 20 percent less than list price right away.

And another thing to note: if the house is in aged listing, which means it’s been on the market more than 60 days.

Remember, that’s actively on the market. If it’s been under contract, that halts that process.

But if it’s been available to bid for 60 days, HUD may take less than that original 11 percent as well. So it doesn’t hurt to submit bids, even if you don’t think they’ll be accepted.

Remember, sometimes you might get a counter offer.

Sometimes HUD will counter you, tell you how much your bid needs to be, it is not a true counter in the sense that you can just accept it and the home is under contract.

You would have to have your agent go back to the system, re-enter the bid, and if there were no other bids and your bid was high enough, HUD would accept that.

With extremely aged listings, over three months, maybe four months, HUD also may take 60 percent, I’ve even heard 50 percent of list price. But those are very aged listings usually in markets that are very slow, very hard to sell homes in.

What are some of the steps that HUD takes to make sure that the HUD property would be insure or not?

HUD has an appraisal done on every home before it’s listed.

The appraiser goes through, determines the value, also notes any repairs for an FHA loan.

If that appraiser thinks there’s less than 5,000 dollars in repairs needed for the home to qualify for FHA, it will be FHA finance-able, insured with escrow.

If they think there’s more than 5,000 dollars in repairs needed to go FHA, that’s when it will be uninsured for FHA.

If it is insured for FHA financing, with or without escrow, an owner-occupant can get an FHA loan on the home.

And if it has an escrow repair, they would determine how much money they need to make those repairs.

Say it needs a new furnace, and the buyer’s inspector estimates it will cost 3,000 dollars to repair that furnace, that amount is added onto the buyer’s loan.

You know, HUD does not pay this escrow, the buyer’s paying it, but it’s added onto their loan. The repairs are made after closing, so after the house closes to the buyer, the repairs will be made by a licensed contractor.

And then the lender will reimburse that contractor out of the proceeds from the loan. If there’s any money left, say the furnace only cost 2,500 dollars, that 500 dollars would go towards paying off principal on the loan.

It would not go directly to the buyer. So the FHA insured with escrow program allows an FHA buyer to purchase a HUD home that would otherwise need repairs and could not go FHA.

The reason HUD does that is because HUD will not make any repairs on HUD homes. Nor will they allow any repairs to be done, except in very rare circumstances.

Those circumstances are if the home is vandalized, or damaged by a storm, and imminent damage will be done to the home or it’s dangerous.

If a window breaks, if there’s a hole in the roof, and, you know, the house is flooding, HUD will come make repairs such as: patching up the roof or tarp the roof, they will replace windows or replace doors if they’re broken in.

But that’s only for items done, after the home has listed, dangerous items.

They will not make repairs to plumbing, they will not make repairs to heating systems.

It doesn’t matter if those repairs are required for your loan or not.

That is their nationwide policy. And it’s very important to know that before you bid on a HUD home.

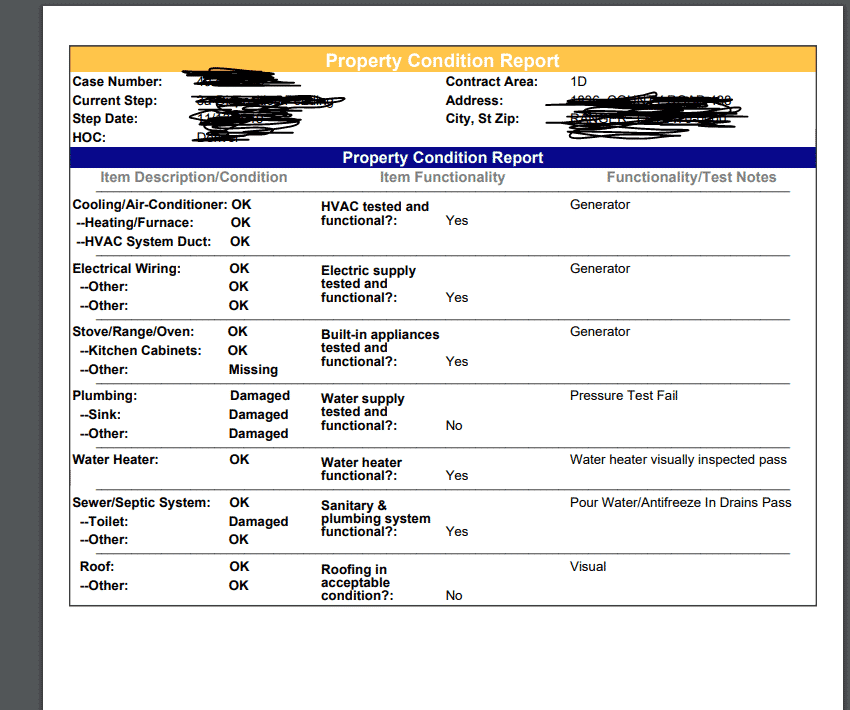

But you’re not going into this completely blind. When you look at the tab called addendum, there will be a form in here called the PCR.

This stands for property condition report. Not only does HUD do an appraisal on every home before it’s listed—and by the way, those appraisals are not available to buyers anymore. They used to be; they are no longer.

If you’re doing FHA, conventional, any type of loan, you will have to get a brand new appraisal. You cannot use HUD’s appraisal, and they will not show it to your lender either. But this shows you what the inspector found on this home.

Now this is not a replacement for your own inspection.

These appraisers many times do not do complete inspections because utilities may not be on, or they might not have access to the roof.

It’s not as complete as having your own inspector who will check out everything for you, and usually have most utilities on.

But it can give you some basic information to help you with your bid.

All right. So right here it will tell you the heating system, cooling system, it says it’s in okay shape. It says they tested it and it’s functional.

This will give you detail information on what was checked and what wasn’t checked. So you will need to go down the list and check to see what is working and what is not working.

This is why you cannot use a HUD inspection in replacement of your own.

You need to get your inspector out there, check out the furnace, get the gas on, make sure everything’s actually working.

Electrical wiring: in the example looks to be tested and reporting, no deficiencies. Again, it’s always best to double check these.

The appliances, they tested those, good physical condition—you never know how long they had them on, what exactly they do in these tests.

Remember, to pay attention to: plumbing and the water systems.

If the plumbing is damaged, HUD will not let you turn the water on for inspections or appraisals.

No exceptions. Doesn’t matter if it’s required for your loan.

This is one of the biggest hiccups that happens when agents and buyers are trying to purchase a HUD home.

If they’re getting a loan, it could be conventional, could be VA, could be USDA—they require the water to be turned on, but the plumbing system is damaged and HUD will not let them turn it on. It doesn’t matter if the lender requires it, HUD will not turn them on.

The deal is going to collapse unless they switch lenders to somebody who doesn’t need the water on.

Now if you’re using FHA, doing an FHA loan, you can escrow the damage and the repairs for the plumbing, and you don’t have to have the plumbing on to get an FHA loan.

That’s the only loan you can use that escrow for. You can’t use it for conventional, you can’t use it for VA, you can’t use it for USDA—only FHA.

So it’s very important to look at this property condition report before you bid and see if you can turn the water on.

In the example: damaged plumbing, does not work. The plumbing system did not hold pressure with applied with an air compressor.

Leaks detected in the crawlspace. So they don’t give us a whole lot of information. HUD does not turn the water, they only use an air compressor to test the system.

If they find leaks, you cannot turn the water on. Don’t think you can get your bid accepted then talk your way into them letting you have an exception because it won’t work.

You’re going to be wasting a lot of time and probably money. In the example report the water heater looks okay.

Again, they don’t turn the water on. So they just basically look at it visually, see if it looks all right. Sewing, sewer system, missing, not functional.

The roof appears to be ok. There is No visible leaks. So this gives you quite a bit of information before you even see the home on what work it needs, what condition it is in.

What are some of the other HUD addendums?

The other addendums, it talks about earnest money guidelines, lead-based paint addendum, and then proper disclosures and repairs.

This, we’ll open up as well. It will tell you what the appraiser found when they did their report. If you are buying a HUD property remember to inspect the property yourself.

Even HUD will tell you, you need to get your own inspector.

When you see repair escrow this is what they are assuming the repairs will cost. Again, you can adjust this if you need to.

If you do inspections and you find the plumbing system is much more damaged, you can raise this amount with 2 bids and a letter from your lender saying why you have to raise it.

If you find more repairs are required for FHA—remember, this is only FHA—you can add them on to here.

And you can take off repairs if you find out something isn’t damaged that HUD lists as damaged.

So you’ve got to be careful. If the roof is 10,000 dollars, you can no longer go FHA with this repair escrow.

You could do FHA 203K rehab loan, but that’s going to be a much more involved, different process than the regular FHA 203B loan with escrow. What about the earnest money guidelines?

All HUD homes have the same earnest money requirements. So if the home is 50,000 dollars or less, the earnest money is 1000 dollars.

If the home is 50,000 dollars and one dollar and over, it’s a 2,000 dollars. So the HUD home could be 400,000 dollars, and it could go up on in dollars for earnest money.

Owner-occupants have a much better chance of getting their earnest money back if something happens with the contract.

If their loan is denied, they will usually get that money back. If they find repairs needed that aren’t listed on the PCR, they will get that money back.

Now if you’re an owner-occupant, you do your inspection, and you find out the plumbing’s damaged on this house, and you ask for your earnest money back because the plumbing’s damaged, HUD is going to say you already knew the plumbing was damaged because it was listed in the PCR, we are not giving you your earnest money.

So you need to make sure that any repairs, any reasons you’re canceling, are different, something you found besides what is on that PCR (Property Disclosure and Repair Information.)

Because HUD assumes you already know about those repairs. If you are an investor, it is much different for earnest money.

HUD assumes you know what you’re doing, you’re experienced.

They will not give you your earnest money back if you find something wrong with the house, even if it’s not listed on the PCR.

You could find out the entire heating system is bad, or you could find mold behind the walls—they will not give you your earnest money back; it will be forfeited.

The only time an investor gets their earnest money back is if they’re getting a loan, and the lender denies them, HUD may give them 50 percent back of their earnest money. May—that’s the sole discretion of HUD.

And if something happens to the house after it goes under contract, like a tree falls on it, someone steals the plumbing, then HUD will probably give the earnest money back to the investor if something happens after the investor gets a contract on the property.

Very important to know about Earnest money with HUD homes. HUD system sounds very complicated,but once you figure out the system, and how it works, it gets easier.

Everything’s the same every time, they have the same policies, each property sold the same way. But it does take a little time to get use to it.

When does HUD typically lower there price on homes?

HUD will lower the price every 35 to 45 days. Usually they lower it to a lower percent, and then they would lower the net bids they would accept when that price is lowered as well.

So the best thing you can do is just make an offer.

In some cases if you submitted a bid that was not accepted to begin with, and HUD lowers their price to a point where that bid would be accepted, they might go back to the buyer and say we will now accept your bid because it meets HUD guidelines.

Your agent has to mark “save as backup” in your offer when they submit your offer. So your agent will know about this, but whenever you submit a bid to HUD always have your agent mark “keep as backup offer.”

It does not hurt you at all, you are not bound by that. If for some reason later on down the road, HUD accepts an offer from you because you marked it save as backup, and you don’t want to buy that house anymore.

All you do is tell HUD, I don’t want to buy it, I’m no longer interested, and they will cancel your bid. No penalty to you.

You have not sent them earnest money, you have not signed anything, so you’re not bound to that little check mark that says save as backup.

Things to remember when you submit your offer.

Remember it’s very easy for your agent to log in, and register, and then they submit an offer. There are a few things that you need in order to make your offer.

You will have to give your social security number, your address information for all the buyers. Remember, HUD will review all bids in those first 10 days,and make a decision the next business day.

If we’re past those days, HUD reviews bids every business day.

So let’s say the home’s been on the market 30 days actively. We would be passed the owner-occupied bid period. That means all bidders are able to bid.

Pay close attention to the submission deadline because the next business day they would review the bid.

And then the bid submission time would tell you how long you had to get your bid in. Now if you’re bidding on a Friday or a Saturday, HUD will accept bids every day up until the next business day.

So if you submit a bid on Friday, they’ll review bids that came in Friday, Saturday and Sunday all at once on that next business day.

If your bid is accepted, you have 48 hours to send all your paperwork into HUD.

HUD will send the contract to your agent, all the disclosures, all the addendums. HUD does not sign any state contracts, any state disclosures, it all has to be HUD documents. That has to be sent in 48 hours, and that’s business hours.

So if your HUD bid is accepted on a Friday, you actually have until the next Tuesday to get your documents to HUD.

Once HUD has your documents, they will review the contract. If it needs work, they will email your real estate agent and tell them what corrections have to be made. Make sure your agent is checking their email frequently.

If not, they will cancel your bid if they don’t hear from your agent in 24 hours. Once they accept your bid, they will sign off on it. And your inspection period will start, which is 15 days. So you have 15 days for your inspection.

Again, if you’re an owner-occupant, you find something wrong that was not listed on the PCR, you can cancel your contract, get your earnest money back.

HUD will not reduce the price for anything you find, so if you’re trying to negotiate with HUD, it won’t work.

You’ll have to cancel your bid and bid at a lower price if you want to buy a home for less than your original bid.

HUD will not make repairs based of your inspection. So it’s all for informational purposes only. If you have to do an appraisal, I suggest doing it at the same time as you’re doing your inspection, especially if you have to have the water turned on.

Because HUD allows a three-day period to have the utilities turned on. And if you have to have the home re-winterized, you will have to pay that 150 dollars up front, schedule your appraisal and inspection at the same time, so you don’t have to pay that 150 dollars twice.

And the buyer can choose their own title company on HUD homes, so you don’t have to use HUD’s tile company.

In fact, you have to use your own title company to close the deal. Again, HUD pays none of those costs.

They don’t closing fees, title insurance—any of that. If you ask HUD to pay some of your closing costs, which you can do in the contract, then you can apply some of that money towards title insurance and other costs, but it will lower your net price to HUD.

What do I need to do to cancel my Hud Contract?

If you want to cancel your contract, you have to use HUD’s cancellation form. Your agent can email HUD, let them know you’re canceling, and HUD will create that form for you. A few things to know about HUD that is very important.

Can I move into or repair the HUD Home before closing?

No! Repairs are not allowed to be made by the buyer under any circumstances. HUD homes are federal property.

That means it is a felony to vandalize a HUD home. And making repairs on a HUD home is considered vandalizing it.

You cannot paint it, you cannot take out carpet, you cannot repair the plumbing, you cannot do anything to the HUD home before you buy it. It is a felony. HUD’s penalties are up to a 250,000-dollar fine and two years in federal prison for violating their rules.

The same goes for trespassing, if you move into the home before closing, you move any items into the home, you start parking a camper in the backyard—that is considered trespassing, punishable by the same penalties.

You have to be with your real estate agent at all times when you’re visiting the HUD home.

It is also considered trespassing if you’re agent gives you the lock box, and you are there without your agent, unaccompanied in the property.

How does HUD properties benefit investors?

Investors can get great deals on HUD homes. Usually, the best way for an investor to buy a HUD home is when they’re uninsured.

That is when the homes need the most work. It’s very hard for owner-occupants to get loans because of all the work needed. And the bit period for owner-occupants is shorter—only five days.

So on that sixth day, HUD will review the bids they may have received from owner-occupants. Investors are encourage to bid on HUD homes on the sixth day as early as possible.

And the reason is, if an investor gets their bid in on the sixth day at say, 6am, and HUD then accepts an owner-occupant’s bid from the previous bid period at 10 a.m. that day.

The home would go under contract with that owner-occupant, but if that owner-occupant cancels, HUD may go back and accept that investors bid before they put it back on the market for other investors, if it meets their requirements.

So it’s a little trick. Many investors gets great deals bidding on the sixth day in the morning because the owner-occupant cancelled.

It’s very common for them to cancel on uninsured homes because they need so much work. Bid early on that sixth day.

The same thing for the insured properties: bid on that sixteenth day; that’s when the investors will get those deals.

If you wait one day, you wait two days, you are probably going to miss out to another investor because they’re going to be bidding as soon as they possibly can.

There is a good chance that HUD homes inventory might be low, but HUD properties can give investors great deals.

Keep in mind many investors are wholesalers and wholesale flipping to other investors. Remember you cannot assign a HUD contract.

Conclusion:

As owner-occupant, you have to live in the home for one year. That’s the requirement: living in the home for a few years means it is your primary residence, you live there more than 50 percent of the time for a few years.

Among other requirements, § 203.37a sets forth time restrictions that make properties that have recently been resold ineligible as security for FHA-insured mortgage financing.

Specifically, § 203.37a prohibits FHA-insured mortgage financing for any property being sold in 90 days or less after acquisition by the seller.

Properties that are sold between 91 and 180 days after acquisition by the sellers to home buyers seeking FHA-insured financing are generally eligible for an FHA-insured mortgage, but are subject to additional documentation requirements to ensure that any increases in the values of the properties are supportable.